They Make Money Even if You Don't

Investors may not realize they are paying for this "hidden fee." This fee is paid to the advisor to acquire more customers, at the cost of the investor's own potential earnings.

Key Takeaways:

The 12B-1 Fee cannot be greater than 1% of a fund's net assets.

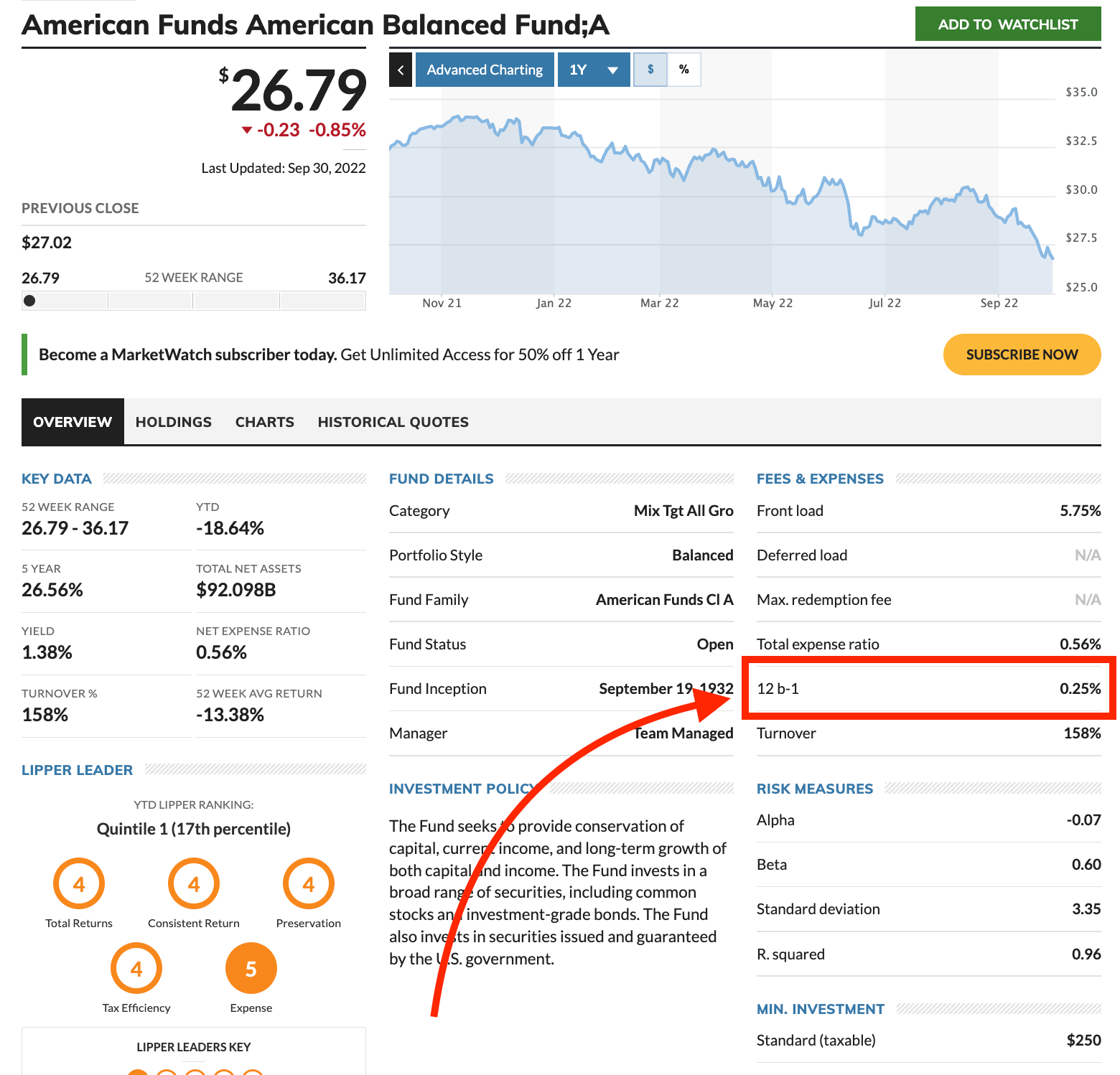

Information on the amount of the funds 12B-1 Fee and what it is used for as included in the funds prospectus.

A 12B-1 Fee is a marketing or distribution fee charged to investors.

Most mutual funds incur sales charges which are paid to brokers for selling the fund.

What is a 12B-1 Fee?

A 12B-1 Fee is a marketing or distribution fee charged to investors by a mutual fund to pay for annual marketing expenses. Information on the amount of the funds 12B-1 Fee and what it is used for as included in the funds prospectus.

This fee is considered an operational expense. It is included in the funds total expense ratio, which is the percentage of the funds average net assets. The total expense ratio also includes the management fee and various other operating costs that the fund incurs. 1

According to the SEC, the 12B-1 Fee cannot be greater than 1% of a fund's net assets and that usually ranges from 0.25 to 1%. In addition, to the 12B-1 Fee, most mutual funds incur sales charges which are paid to brokers for selling the fund:2

If the sales charge is paid when the fund is purchased, the fund is called a front-end load fund.

If the sales charge is paid when the investor sells the fund, it is a back end load fund.

Sales charges are not part of the funds operating expenses. They are paid from the initial investment in the case of a front-end load or from the proceeds of the sale of the fund in the case of a back-end load. Back-end load charges sometimes declined over time so the longer the fund is on, the lower the charge when it is sold.

Some funds which are known as 12B-1 Plan Funds can use fund assets to pay the distribution charges for the fund and therefore do not charge a sales fee. These funds assess an annual fee based on the current value of the fund. This is sometimes known as a hidden load because it is not as obvious to the investor as a sales charge might be. The fee itself may be known as the level load because it is assessed at the same percentage each year. The amount of the fee will increase as the value of the fund increases, however, so these charges can significantly impact the return of the fund.

All expenses related to the fund are disclosed in the prospectus of the fund. The prospectus document must be supplied to the investor prior to or at the time of purchase.

Investors should read and understand new perspectives (particularly the sections that refer to fees in sales charges). Identifying those funds, which have the most attractive relationship between fees and performance can be very beneficial in terms of the return on investment.

How to avoid 12B-1 Fees according to Rowling and Associates:3

There are a couple things you can do to protect your investments from being subjected to these “hidden” fees. For one thing, when researching mutual funds, look for those that have a low expense ratio. These will often be index or passively managed funds. If you aren’t exactly sure what constitutes a low expense ratio, you can also look into the mutual fund’s prospectus, which should be available to you. In the section for “shareholder fees”, it should indicate how much is charged for marketing and distribution. As a reminder, the typical 12B-1 Fee is 0.25%, and the maximum charge for 12B-1 Fees is 1% annually.

Of course, the easiest way to protect your investments is to work with a fiduciary financial advisor – or, even better, a fee-only fiduciary advisor. Fiduciaries are legally obligated to always act in their clients’ best interests. Fee-only firms do not earn commissions on any recommendations given to their clients. So, in this instance, a fee-only fiduciary advisor would not have any reason to recommend a higher-cost mutual fund class with a 12B-1 Fee because there would be no benefit for them, or their client.

If you are not sure whether your financial advisor is a fiduciary, ask them! If they are not, consider switching to someone who is. You could save yourself a lot of money in the long run.

https://www.investopedia.com/terms/1/12b-1fees.asp

https://www.investopedia.com/terms/i/investmentcompanyact.asp

https://www.rowling.com/2020/02/27/hidden-12b-1-fees-can-pack-a-punch/